Retirement isn't a spreadsheet.

It's a journey.

WhenIm64 is your guide through every critical decision — Medicare enrollment, Social Security timing, Roth conversions, and RMDs. With reminders when it's time to act, and course corrections when life changes.

Built for people navigating retirement who want clear guidance, not another calculator.

No SSN required. No bank credentials. No credit card to start. How we protect your data →

Your turn-by-turn retirement guide

Most retirement apps show you a model. WhenIm64 tells you what to do next.

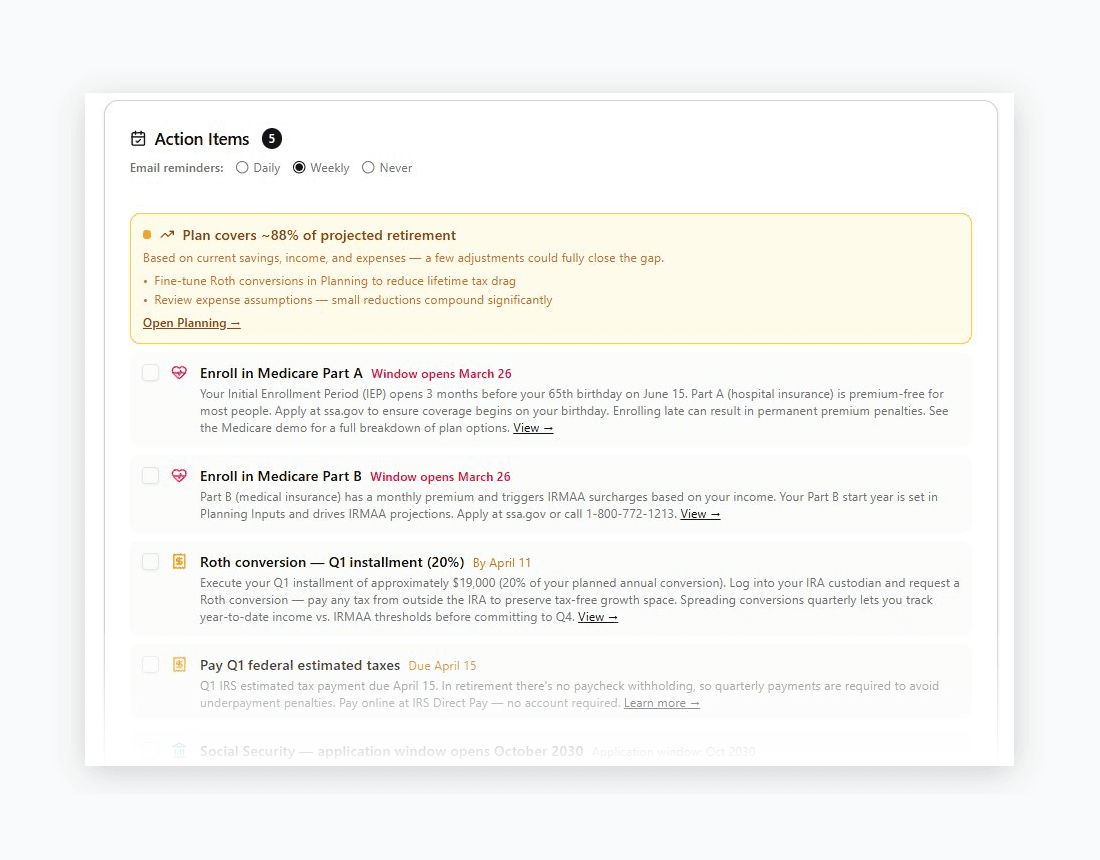

Action items with real deadlines

Your dashboard surfaces what needs attention now — Medicare enrollment windows, quarterly tax payments, Roth conversion installments — so nothing slips through the cracks.

Retirement Dashboard →

Your retirement journey at a glance

The milestone timeline shows where you are, what's coming, and the strategic windows — like the Tax Valley — that define your plan.

My Plan →

Guides for the decisions that matter most

Deep, personalized guidance on Medicare, Social Security, and tax strategy — not generic advice, but answers grounded in your specific ages, income, and accounts.

Healthcare Guide →The retirement window most people don't know they have

If you were born after 1960 and plan to retire before claiming Social Security, you're sitting on one of the most valuable — and underused — tax opportunities in retirement planning.

It's called the Tax Valley.

Between the day you retire and the day your Required Minimum Distributions begin at age 75, there's a window where your taxable income drops dramatically. No W-2 income. No Social Security yet. No forced IRA withdrawals. For many people born after 1960, this window is 10 years or longer.

Every dollar you convert from your IRA to Roth during this window is taxed at your lowest rate — often the 12% or 22% bracket. Leave it unconverted, and RMDs will force those withdrawals later at whatever bracket you're in then, with no choice about timing.

SECURE 2.0 pushed RMD age to 75 for anyone born after 1960. Combined with later Full Retirement Ages, the Tax Valley has quietly become one of the largest planning opportunities a generation of retirees has ever had — and most financial apps don't explain it clearly.

Early

care

FRA

Max

Start

Begins

Early retiree profile · Tax Valley spans retirement date to RMD start at age 75

WhenIm64 shows you exactly how wide your window is, how much to convert each year, and when the window closes.

Life changes. The guide adjusts.

Traditional retirement planning asks you to predict the future accurately.WhenIm64 doesn't.

Markets move. Expenses shift. Plans change. A retirement plan that gets updated quarterly and course-corrected as life happens will outperform a perfectly modeled plan that gets opened once and forgotten.

That's why WhenIm64 is built around a quarterly review — a short walkthrough that keeps your plan honest without requiring you to rebuild it from scratch. Each quarter, the guide checks in: are you on track, has anything changed, is there an action item coming up?

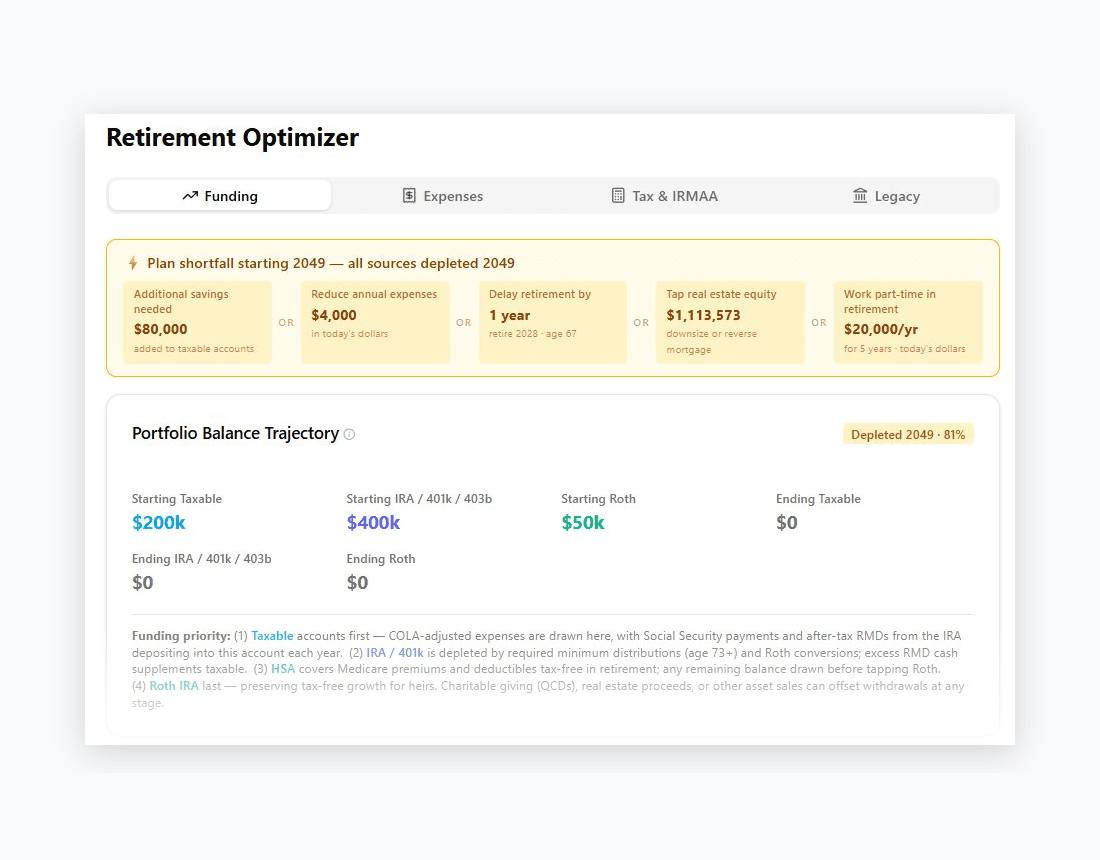

When something does fall short, WhenIm64 calculates five concrete ways to close the gap — additional savings, expense adjustment, delayed retirement, real estate equity, or part-time income — so you're never staring at a red warning with no path forward.

- Additional savings — the lump sum that puts your plan back on track

- Reduce expenses — how much less per year in today's dollars

- Delay retirement — extra working years needed, with the new target date

- Tap real estate — available home equity via downsizing or reverse mortgage

- Work part-time — annual income needed for the first 5 years of retirement

Not a set-it-and-forget-it calculator. A coach that checks in.

Our Story

Built by someone who learned all of this the hard way.

WhenIm64 was created by a recently retired engineer who was blindsided by the complexity of Medicare enrollment, IRMAA surcharges, and retirement tax planning.

Between an inbox flooded with 200+ Medicare mailers and hour-long hold times with the SSA — including a representative who had “never heard of IRMAA” — the decision was made to build the tool that should have existed all along.

WhenIm64 is the result: a clear, honest guide through the financial decisions that define retirement. Built for people who deserve better than junk mail and hold music.

It covers about 80% of what a retirement specialist would cover, at a fraction of the cost — and it tells you clearly when your situation calls for professional advice.

AI that knows your plan

Ask plain-English questions and get answers grounded in your specific numbers — ages, income, accounts, state, and retirement timeline.

AI Retirement Assistant

Using James & Linda's plan data

✅ James: Claim at Age 70 (year 2031) — Keep your current plan

Your $650k savings comfortably covers the 4-year bridge. The break-even is age 80.4 — given your planning horizon to 90, you'd collect ~$141,000 more in cumulative lifetime benefits by waiting vs. claiming at 62. More importantly, delaying preserves your tax valley for $450k+ in Roth conversions.

✅ Spouse: Claim at Age 70 (year 2032) — Keep current plan

The survivor benefit is critical: if James predeceases spouse, she steps up to your higher $36,000/yr benefit — the longer you delay, the larger that survivor protection.

AI Retirement Assistant

Using James & Linda's plan data

Here's a category-by-category breakdown for a married couple in Austin, TX, retiring in 2027. Adjusted for local cost of living — Texas has no state income tax but higher property insurance and utilities.

Everything in one place

Most retirees leave significant money on the table from missed deadlines, early Social Security claims, and avoidable taxes. WhenIm64 makes the right answer clear — and tells you when to act on it.

Action Items & Reminders

Your dashboard surfaces what needs attention now — Medicare enrollment deadlines, quarterly tax payments, Roth conversion opportunities, and plan funding alerts — with email reminders so nothing slips.

Roth Conversion Optimizer

Fill your tax bracket intelligently each year. Visualize the full projection — IRA balance, Roth growth, RMDs, and IRMAA surcharges — across your entire retirement.

Social Security Timing

Model your Full Retirement Age, delay credits, spousal benefits, and survivor benefits. See the lifetime break-even between claiming at 62 vs. 70.

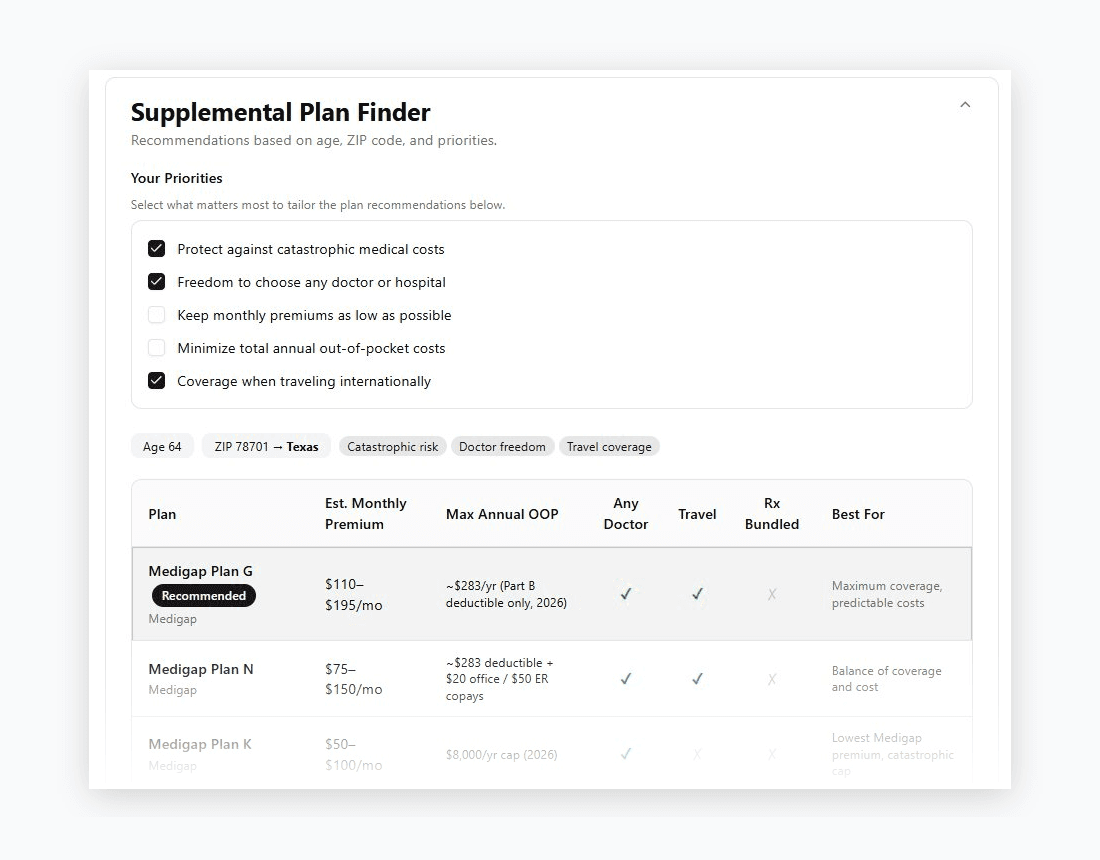

Medicare Planning

Compare Medigap and Medicare Advantage side by side. Find Part D drug plans for your state, track your enrollment status, and never miss an enrollment window.

Quarterly Tax Estimates

In retirement there's no paycheck withholding. Know your federal and state estimated tax payments each quarter so you never face an underpayment penalty.

RMD Planning

Required Minimum Distributions begin at 73 or 75 (depending on your birth year) and rise every year. Model the impact on your tax bracket and see how Roth conversions reduce future RMD burdens.

How WhenIm64 compares

| Feature | WhenIm64 Free | WhenIm64 Premium | Boldin (NewRetirement) | ProjectionLab | Empower |

|---|---|---|---|---|---|

| Price | Free forever | $99 / year | Free / $144 per year | Free* / $129 per year | Free |

| Designed for non-experts | Steep learning curve | Steep learning curve | |||

| Turn-by-turn guidance through every retirement decision | |||||

| Proactive alerts when it’s time to act | |||||

| Email reminders so nothing slips | |||||

| Quarterly course-correction | |||||

| Social Security timing | |||||

| Roth conversion optimizer | |||||

| Tax Valley guidance | |||||

| IRMAA management | |||||

| Medicare planning & enrollment guidance | Basic only | ||||

| RMD planning | Basic only | ||||

| Estimated quarterly taxes | |||||

| AI retirement assistant | |||||

| Brokerage connection | |||||

| Data saved between sessions | Free tier does not save data |

Simple, transparent pricing

Start free — upgrade when you want the full experience.

Free

Everything you need to start your retirement journey.

- Dashboard with your full retirement snapshot

- Social Security timing and claiming strategy

- Medicare enrollment tracking and plan comparison

- Roth conversion optimizer with IRMAA management

- Quarterly estimated tax calculator

- RMD projections and legacy planning

- Educational retirement content and guides

Premium

or $99 / year save 17%

For investors who want the full picture.

- Everything in Free

- Ad-free experience

- AI retirement help assistant

- Brokerage portfolio import and sync — handled securely via SnapTrade; WhenIm64 never sees your account credentials. Learn more →

- Action item email reminders

The free plan is supported by Google AdSense — a straightforward trade rather than a hidden business model. Premium removes ads entirely and is priced to cover its actual costs: AI processing, brokerage data access, and email delivery. No markup beyond that.

Your guide is ready when you are.

Free to start. No credit card. Takes about 10 minutes to set up your full retirement profile — and the guide goes to work immediately.

No SSN ever|No brokerage credentials|Your data is never sold|Security & Data Protection →