When I first started building the Medicare section of WhenIm64, I built a simple plan selector for choosing between Medicare Advantage and Medigap coverage, then selected representative plans that met the user's needs. This was straightforward, so I moved on to Part D plans, which was a different story entirely.

Part D turned out to be extremely complicated, with many independent variables driving cost: premiums, deductibles, different rules for what you pay during the deductible period, and drug prices that vary by plan, pharmacy, and zip code. What surprised me most was discovering that the Inflation Reduction Act, which genuinely transformed Part D for the better, had also made the decision harder to navigate, not easier.

The IRA Changed Everything (And That's Mostly Good)

Before 2025, the Part D horror stories were real. People on expensive specialty medications could face tens of thousands of dollars in annual drug costs. The infamous "donut hole" coverage gap created bizarre incentives. There was no ceiling on what you might owe.

The Inflation Reduction Act fixed the most serious problem: starting in 2025, no Medicare beneficiary pays more than $2,000 out of pocket for covered Part D drugs in a year (rising to $2,100 in 2026, indexed for inflation). For someone on an expensive biologic or cancer medication, this is life changing.

Many of the high-premium drug plans existed for one reason: to protect subscribers from catastrophic out-of-pocket expenses that were previously uncapped. Now that the cap is in place, those plans make no sense at all. They are still being offered, but they just clutter up the plan finders and comparison tools. Skip them.

Capping the downside also compressed the difference between plans. When one plan could cost you $3,000 more than another in a bad year, plan selection was high stakes and the math was obvious. Now, for most people, the difference between the best and worst plan choice is probably under $500 annually. The stakes got lower, but the decision got murkier.

The Problem No One Talks About

Here is my most embarrassing discovery: I made the wrong choice on my own Part D plan during last year's open enrollment.

I anchored on the premium. I saw a plan with a $10/month lower premium, noted the $590 deductible on the plan I was comparing it to, and picked the lower-premium plan. Seemed reasonable.

It wasn't. When I finally ran the numbers properly for my specific drug list, the plan I didn't pick was cheaper by several hundred dollars annually. The per-drug monthly costs on my specific medications were meaningfully lower, and the deductible on the plan I chose hit me directly in a way I hadn't anticipated.

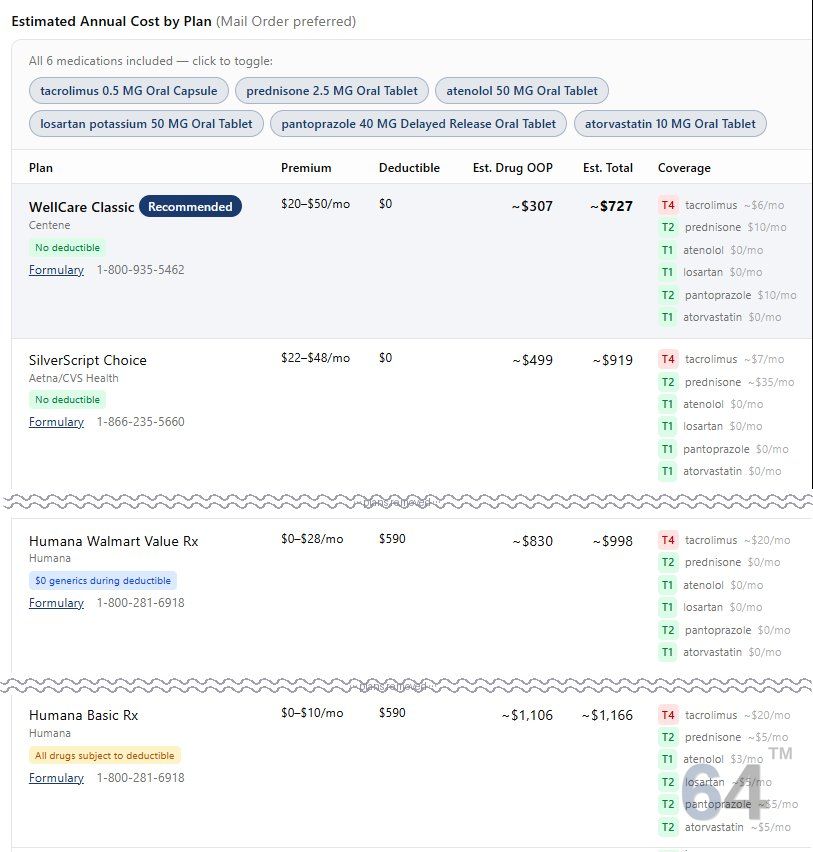

This is a trap that catches a lot of people. The premium is the most visible number. But the only number that actually matters is the estimated annual total cost for your specific drug list. Everything else is just an input to that calculation.

What the Plan Finder Won't Tell You

The obvious place to compare plans is the Medicare Plan Finder at medicare.gov. Enter your drugs, compare plans, pick the cheapest. Except it is not that simple.

The Plan Finder will show you copays and coinsurance for your drugs after you have met your deductible. What it will not show you is the negotiated price you pay for those same drugs during the deductible phase, before your plan starts sharing the cost. That negotiated price depends on your specific plan, your specific pharmacy, and your zip code. It is not published anywhere in a way that is easy to find or compare.