Everyone knows the basic argument for delaying Social Security: bigger monthly check, 8% annual credits between full retirement age and 70, break-even somewhere around 82. Most financial advisors know this. Most SS calculators model it. The advice to delay is correct.

What almost nobody models is what delaying does to the rest of your tax picture.

The Tax Valley

When you retire before Social Security begins, your taxable income drops sharply. No more W-2. SS not yet started. If you have not yet hit RMD age, your IRA sits untouched. For many retirees this creates a window, sometimes several years wide, where taxable income is at its lowest point in the entire retirement plan.

During this window, the standard deduction plus the lower federal tax brackets give a married couple roughly $130,000 of income per year that can be recognized at 12% or below. This is the Tax Valley. It is one of the most valuable planning windows in retirement, and most people either don't know it exists or don't use it deliberately.

Claiming Social Security early closes part of that window. Every dollar of SS income that flows in during the Tax Valley years fills bracket space that could otherwise be used for Roth conversions at the lowest rates you will see for the rest of your retirement.

Why This Matters More Than the Bigger Check

Here is the problem with leaving a traditional IRA untouched through the Tax Valley and beyond. The IRA keeps growing. RMDs starting at 73 or 75 force distributions as ordinary income, on top of Social Security that is now fully in payment, on top of investment income. The marginal rate on those forced distributions is often 22% or higher, and you have no choice about the timing.

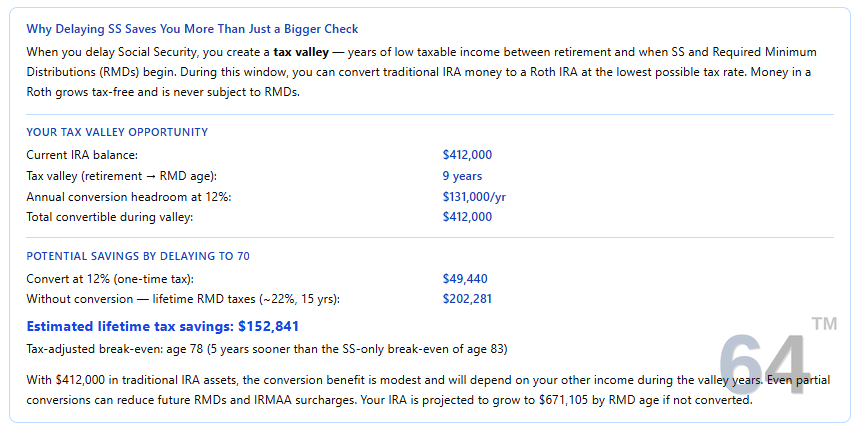

Contrast that with what is possible during a long Tax Valley. Here is what the analysis looks like for a couple retiring at 66 with a $412,000 traditional IRA and a nine-year Tax Valley:

The tax-adjusted break-even for this scenario is age 78, five years earlier than the SS-only break-even of 83. The Roth conversion savings are doing that work. The difference compounds tax-free for the life of the plan with no future RMDs.

The Tax Valley is not just a quieter period in the retirement income plan. It is a one-time opportunity to reposition pre-tax money at the lowest rates you will ever see. Once Social Security starts and RMDs begin, that window closes permanently.

What Delaying Social Security Actually Buys You

When you delay SS from 62 to 70 and retire in between, you are not just buying a bigger check at 70. You are buying additional Tax Valley years. Every year you delay is another year of low-income space for Roth conversions, capital gains harvesting at the 0% rate, and IRMAA management before Medicare costs escalate.

The traditional SS break-even analysis, which puts the crossover at around age 82, only counts the bigger check. It ignores the value of the additional Tax Valley years created by the delay. When you factor in the Roth conversion savings those years enable, the tax-adjusted break-even comes several years earlier than most people expect.

When It Makes Sense

This logic holds most strongly for couples with meaningful traditional IRA balances where the portfolio can comfortably cover expenses during the delay period. For singles, individual longevity expectations matter more since there is no survivor benefit to consider. For households with small IRA balances, the Roth conversion opportunity is more modest and the analysis simplifies.

The core question is not just "can I afford to delay?" but "what am I doing with the Tax Valley years if I do?"

Most people have not been shown this framing. Standard SS claiming tools optimize the benefit amount in isolation. They do not model what the claiming decision does to IRA balances, future RMDs, or the Roth conversion window. Treating those as separate decisions rather than one integrated plan is where most of the opportunity gets left on the table.

The WhenIm64 SS Claiming Wizard models the full picture: affordability, Tax Valley length, Roth conversion impact, and the tax-adjusted break-even. It is free for all users.

Ben Sprachman is the founder of WhenIm64.ai, a retirement planning tool for people navigating retirement. He is not a financial advisor or tax professional. This article is for educational purposes only. Consult a qualified tax advisor for guidance specific to your situation.