I stumbled onto this problem while testing code.

I was implementing the RMD scheduling feature of WhenIm64, the part of the app that calculates required minimum distributions for each IRA account and surfaces them as an annual action item. I tested one case based on my wife's inherited IRA and it seemed simple enough. Her mother passed away in 2015, and since then my wife gets a small distribution check every January from the brokerage.

But when I added a second test case, another inherited IRA from someone who died in 2020, the model produced a number in 2030 that I had to read twice. I thought Claude Code had made a coding error. Claude insisted the data was correct.

I started researching. This is what I found:

A Tale of Two Rules

To understand what's coming, you need to know about a law that changed in 2020.

Before the SECURE Act of 2019, inheriting an IRA came with a powerful planning tool called the stretch IRA. If you inherited a traditional IRA from a parent, you could take distributions based on your own life expectancy, spreading the tax liability over decades. A 55-year-old who inherited a $300,000 IRA in 2015 might take small annual distributions over 30+ years, keeping each year's taxable income modest while the remaining balance compounded tax-deferred.

My wife's inherited IRA works exactly this way. Her mother died in 2015, before the SECURE Act. The distributions are calculated annually using the IRS Single Life Expectancy table, the factor decrements by 1.0 each year, and the account gradually depletes over her remaining life expectancy. Predictable, manageable, no surprises.

The SECURE Act ended this for most people. For IRAs inherited from people who died on or after January 1, 2020, most non-spouse beneficiaries now face a hard deadline: the entire inherited IRA must be withdrawn by December 31 of the tenth year after the original owner's death.

Congress sold this as a revenue acceleration measure. The policy argument was reasonable. The execution created something Congress and the IRS apparently didn't model carefully together: a structural time bomb embedded in the math.

The Math Nobody Explained

If the original owner had not yet started taking RMDs when they died, there are no annual distributions required from the inherited account. You just have to empty it and pay taxes within 10 years. If the original owner was already taking RMDs, the IRS requires annual distributions from the inherited account throughout the 10-year period as well.

Either way, the problem is the same. Those required annual distributions are calculated using the Single Life Expectancy table, which was designed for lifetime distributions spread over decades. A 55-year-old beneficiary would have a life expectancy factor of roughly 31.6, meaning the annual required distribution is about 3% of the balance. That formula was built to last 30+ years, not 10.

Applied to a 10-year window, those small distributions barely dent the account balance. The account keeps growing. By year 10, the remaining balance can actually be larger than the original inherited amount. You would think that following the IRS-mandated minimums would naturally spread the tax burden across the decade. It doesn't. Not even close.

The Number That Stopped Me

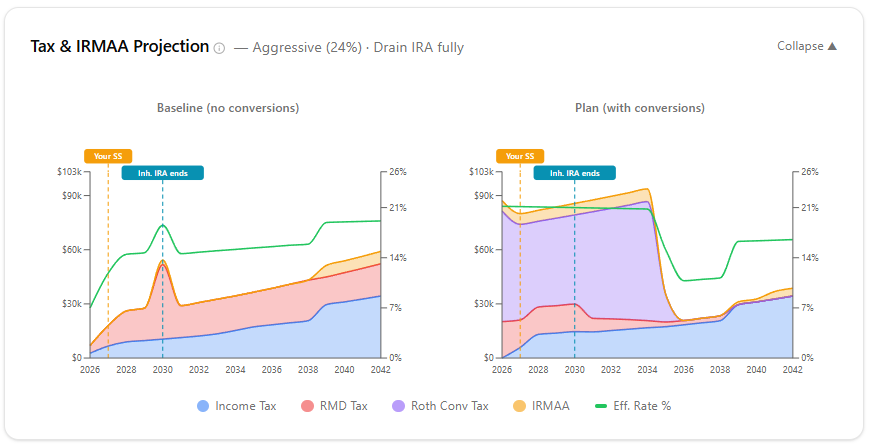

WhenIm64 has a reminder system that prompts you to act when things need to happen: apply for Medicare, file estimated taxes, take your RMD, etc. I was building the inherited IRA piece of that. The wizard confirms the prior year-end balance and calculates what the IRS requires for the current year.

Here is the scenario I tested. A spouse inherits a $175,000 traditional IRA in 2020 from a parent who was 76 at death and already taking RMDs. With the date set to 2026, the wizard calculated a required distribution of $9,375. Small, manageable, easy to absorb.

Then I set the date to 2030 to simulate the final year, when the account must be fully drained.

The wizard showed $178,512. The entire remaining balance, as a single ordinary income event in one tax year.

That was not a bug. The account had continued to grow for nine years while the small required distributions barely touched the principal. Everything left hits in year 10.

For a typical couple in their late 60s or early 70s in 2030, that $178,000 stacks on top of income that might already total $150,000 to $200,000 from their own RMDs, Social Security, and investment income. Total AGI in that single year: potentially $350,000 or more. Multiple IRMAA tiers breached. Tax brackets pushed to 32 or 35 percent on a significant portion. Medicare premiums spiking. A tax bill that looks nothing like any other year in the retirement plan.